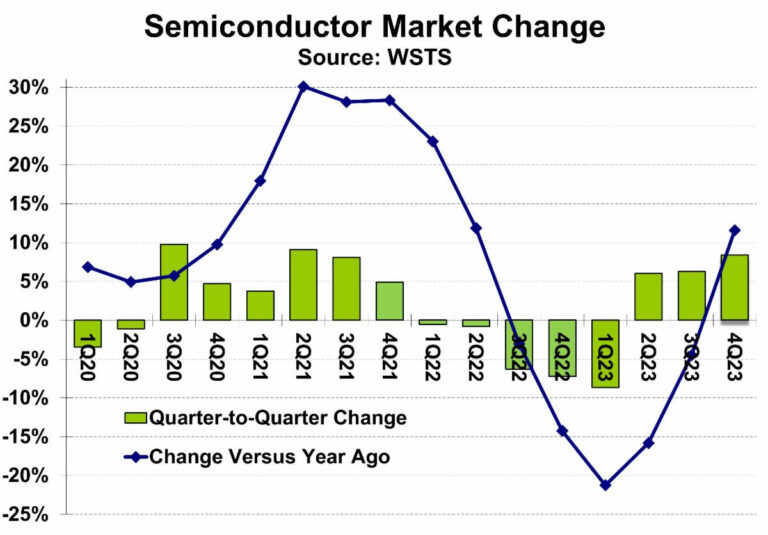

Data from WSTR reveals a sequential increase of 8.4% in global sales of semiconductor components last quarter, pushing the annual comparison revenue up by 11.6%. After five consecutive quarters, this is the first demonstration of a positive momentum, signaling prospects for market growth.

Sequential Revenue Growth: A Look at the Records

According to SemiWiki, which complied the WSTS statistics, the sequential revenue dynamics of global semiconductor components market participants in the fourth quarter broke some records. An 8.4% increase was recorded, the second-highest, following the second quarter of 2021’s 9.1% rise. In 20 years, this is the highest result from the transition from the third to the fourth quarter, a record rivaled only by the fourth quarter of 2003’s 11% increase.

The Driving Force: Memory Chip Segment

The main catalyst for the market revenue growth last quarter was the memory chip segment, driven by the high demand for HBM for computational accelerators, and the resulting price increase for other types of memory chips. Samsung, SK hynix, and Micron saw sequential revenue increases in the fourth quarter of 49%, 24.1%, and 17.9%, respectively. On average, there was a 33% rise in revenue for the three manufacturers in this period. The weighted average revenue growth for the 12 largest sector companies not engaged in memory production was 4% sequentially last quarter.

Outstanding Companies Outside the Memory Segment

Outside the memory sector, MediaTek, Qualcomm, and NVIDIA all saw substantial sequential revenue growths of 17.7%, 14.2%, and potential 10.4% (totaling $20 billion), respectively. However, seven non-memory producing companies did experience a sequential revenue decrease, worst performers being Infineon (-10.2%), Texas Instruments (-10%), and Analog Devices (-8%).

Memory Producers: Positive Projections Amidst Negative Market Trend

Notwithstanding, the first quarter of this year will primarily see a negative sequential revenue dynamics for semiconductor sector companies, with the exception of memory manufacturers like Micron, who anticipate a 12.1% revenue increase. Samsung and SK hynix did not share their forecasts but are hopeful in the face of high demand for their products. Nine non-memory producing companies predict a sequential revenue reduction from 2.8% (Infineon) to 17.6% (Intel) this quarter due to overproduction, low demand in certain market segments, and seasonal influences.

Different Directions: Smartphone and PC Segments

Market trends for end devices last year varied. The smartphone segment saw a reduction of 3.2% in the physical supply; however, IDC experts expect a 3.8% growth this year. Memory manufacturers and mobile processor developers MediaTek and Qualcomm will thrive from this. The supply volumes of the PC segment fell by 14% last year, but a gain of 3.4% is expected this year, benefiting memory manufacturers, CPU suppliers Intel and AMD, and NVIDIA.

Potential Close: The Automotive and Industrial Automation Segments

The automotive market seems to have exhausted its growth potential for this year with a 9% sales volume increase in cars last year and an expected fall of 0.4%. Demand has surpassed the car market supply, as customers have so far satisfied their appetite since the end of the pandemic. There’s also an expected slowdown in chip demand in the industrial automation segment from last year’s 2% to 0.3%, likely affecting the dynamics of STMicroelectronics, Texas Instruments, Infineon Technologies, NXP Semiconductors, Analog Devices, and Renesas Electronics revenue.

WSTS Forecasts: Year 2024

WSTS forecasts indicate a 44.8% rise in memory suppliers’ revenue this year and a meager 6.5% for other semiconductors market participants. Overall, a 13.1% monetary increase is expected in the global semiconductor components market by the end of 2024. Gartner specialists predict a 66% revenue increase in the memory segment and a 16.8% market-wide increase.